To keep themselves grounded in how much they spend, students may resort to saving their earnings for the future. Junior Claire Herndon regularly follows a detailed budget plan to help her in managing her income.

“When I get paid, I try to put at least 20 percent of what I make into savings. I give 10 percent to my church, and I put the rest in my debit account,” Herndon said. “I do this because realistically, if I don’t have a savings plan, I’ll never save, ever.”

Junior Megan Kelly believes there’s a variety of students at RBHS who have differing abilities in managing money. To Kelly, the characteristics and habits depend on the person. She believes there are people who are good with money and those who are not, depending on the environment and situations they are accustomed to.

“I think a lot of it comes from the fact that there are a lot of well-off families at our school, and I’m not saying that is a bad thing,” Kelly said. “It’s just that some kids haven’t really had to deal with what it’s like to save money and not have it always readily available.”

According to www.foxbusiness.com, 87 percent of teens admit they don’t know much about personal finance in a study by ING Direct. In order to assist students who haven’t had exposure to proper budgeting, personal finance instructor Stacy Elsbury said the course follows the practices of financial gurus to teach students quick tips to save their money.

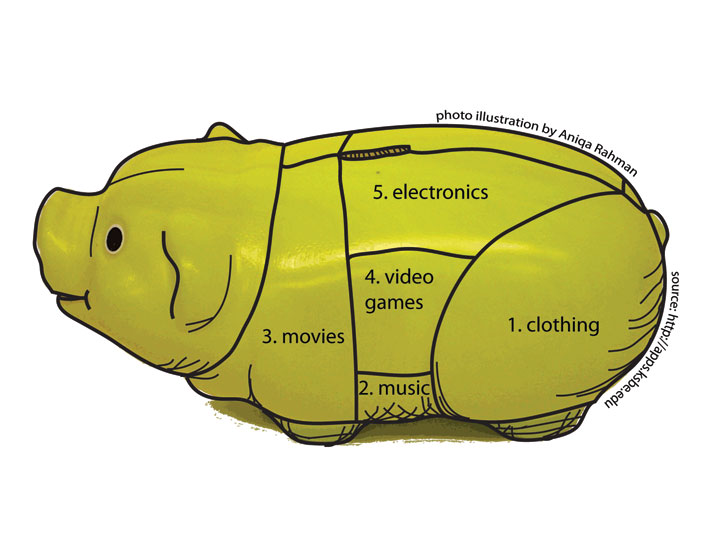

“Students work through a budgeting simulation where they are given a specific career and salary and then have to determine how to divide up their money accordingly. We share basic guidelines such as allocating roughly 10 percent for saving, 25 to 35 percent for housing, 10 to 15 percent for transportation and 15 to 20 percent on food,” Elsbury said. “If you don’t have a plan, then you are more likely to go with whatever feels best at the moment or impulse spending, and that can leave you experiencing buyer’s remorse. Living with a budget is to live with intentionality.”

Herndon admits even she is an impulsive shopper, along with 23 percent of American teens according to www.aboutschwab.com. But Herndon agrees with Elsbury’s advice, and believes students without a savings plan can easily fall into a compulsive mindset. With restaurants so nearby, RBHS students are often persuaded by their peers to go out for lunch, according to Herndon.

“[Students] have no idea what to expect in the future. We don’t think about it,” Herndon said. “We live in the now. We make decisions to go out to lunch daily when we could be saving for college. We look at it like, ‘College is in two years, but I’m hungry now.’”

Sometimes it can be difficult to look so far into the future when it seems as though the money can be better spent now, Kelly said. Rather than frequently spending the majority of her personal cash on food, Kelly pays for her own clothing items when she shops from time to time.

“I spend most of my money on clothes because it’s one of my outlets and it’s what’s important to me,” Kelly said. “I feel better and more confident when I like what I am wearing. I don’t spend a fortune by any means because I try to find deals and still find cute stuff that I can wear a lot.”

Even though Kelly watches how much she spends, Elsbury still suggests that students set money aside for their future, regardless of how tempting shopping now may be.

According to www.foxbusiness.com 83 percent of teens don’t know the basics of managing money, and Elsbury has seen students struggle with saving money because of the absence of a goal to save for, or even not having a measurable income to budget, which negatively impacted their future.

“Money management is like any other good decision we must make for ourselves,” Elsbury said. “Even though we know we need to do it, we sometimes have a hard time controlling ourselves.”

Because of encouragement from her parents to pay for her own purchases, Kelly believes she has mastered the art of self control and is smarter when shopping. Part of the reason Kelly believes she is able to control herself when spending money because all of her money is from savings and earnings from work and has never received an allowance. Students will never learn to budget and manage their money properly by just receiving cash from their parents, Kelly said.

“I think it’s a good idea to not have an allowance and learn what it’s like to make and save your money,” Kelly said. “You wouldn’t necessarily be completely on your own, but [you would] at least be getting an idea of what the future will be like [managing your own money].”

Based on a research study at Ohio State University, 50 percent of teens get a median of $50 a week straight to their pockets. Having an allowance and not being independent with finances in high school is something Herndon believes will cause students to struggle when budgeting their money now and even in their future.

“If your parents pay for all your gas and give you money every time you ask to go shopping, you don’t learn the value of money. I was raised knowing I’m supposed to save and give, so that’s what I do,” Herndon said. “You spend your money differently if it’s yours, so if your parents just hand you money, you’re never going to learn to be wise with it.”

By Manal Salim